Among banks and FinTechs, there’s recognition of the value inherent in receipt data.

That granular detail can help forward-thinking firms craft and offer more customized services and products to their customers.

The report “Meeting the Need for Item-Level Receipt Data: How Integration Enables Innovation,” a PYMNTS and Banyan collaboration, found that 41% of companies are already using this information to support operations. Integrating receipt-level data, at a high level, enables these providers to track consumer spending and offer loyalty and rewards programs, among other innovations.

PYMNTS surveyed 351 executives representing financial institutions (FIs) with at least $5 billion in assets and FinTechs with at least 1 million active monthly users.

These companies know there’s a real need to be innovative. Seventy-two percent of companies surveyed said they believe consumers would switch to firms that provide solutions based on the use of receipt data.

On the provider side, receipt data allows merchants and banks to make more accurate product and service recommendations. At present, 40% of companies said that tracking consumer spending behavior is the most challenging. Fifty-eight percent of firms using receipt data to streamline expense management are the most likely to find it difficult to integrate with existing card-linked offer programs.

But it’s no easy task to integrate that data in ways that can help categorize spend and be used in new product and service development efforts. To use receipt data, firms need to implement data-related capabilities.

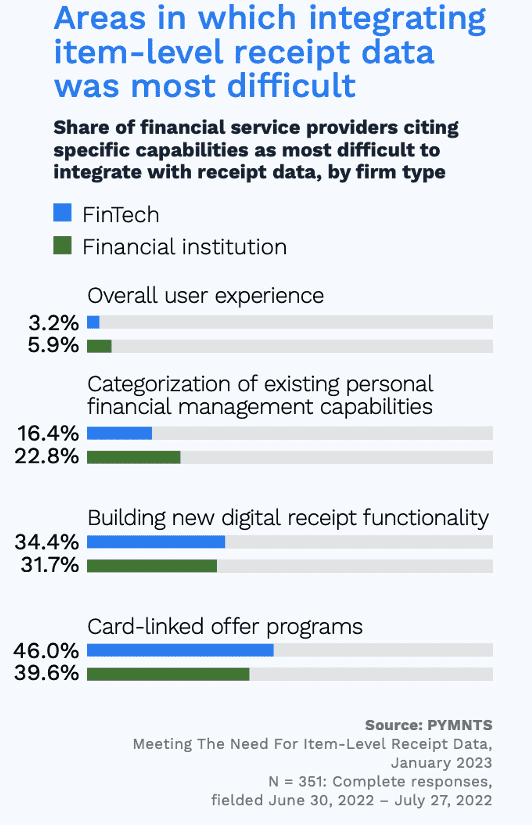

Forty-eight percent of FIs said they consider data standardization to be a key requirement when using item-level receipt data. And 46% of FinTechs said they believe integrating receipt data into their existing loyalty and card-linked offer programs is their most difficult challenges. A significant percentage of all firms — 44% — said they believe that integrating receipt data into their existing card-linked offer programs is the most difficult challenge.

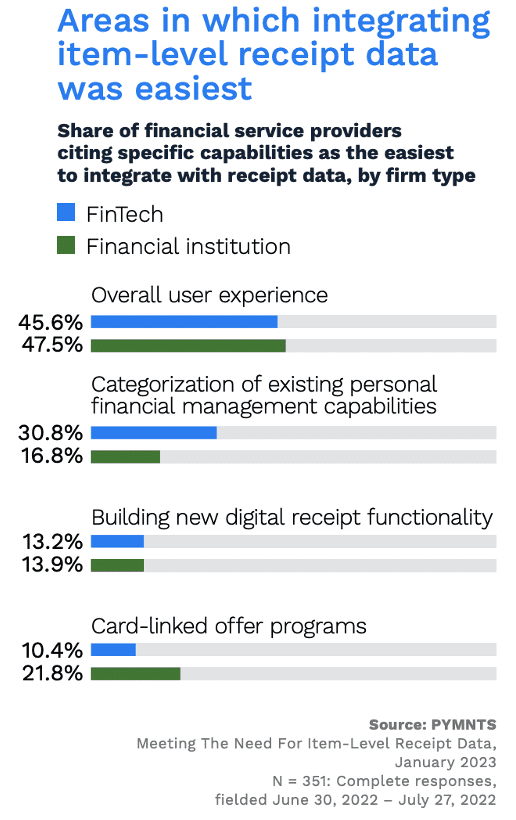

These companies stated that integrating data into the overall user experience is among the “easiest” capabilities.

In terms of where the aspirational goals of harnessing the data might lie is tracking spending behavior. Item-level data gives consumers a better understanding of their spending behavior. The richer data presented to them can help correctly identify food purchases and fuel transactions.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More