Nebraska’s farmers and ranchers, and the state leaders they complain to, are intimately familiar with rural residents’ beef about agricultural property taxes.

They face heftier tax bills than homeowners or many business owners — no matter what they get for their crops or livestock — because they must own lots of land to produce them.

And their tax bills keep rising, seemingly without end, they add.

A new Telegraph analysis focuses on the second premise, days before 2022 property tax bills arrive in Lincoln County property owners’ mailboxes.

This story launches an expansion of our annual “budget season” coverage. We’re adding three anonymous sets of ag properties across the county to the three sample North Platte homes The Telegraph has featured since 2018.

People are also reading…

Using publicly available tax and valuation figures, we set out to find whether Nebraska’s 25-year-old tax-rate and budget lids and a trio of state property tax credits have dented tax bills for these three producers.

The numbers show they have — but their tax bills grew a lot anyway.

Among our key findings:

Even with the three tax credits, they saw their net tax bills after the credits rise between 37.5% and 77.4% from 2012 to 2022.

Their tax relief was minimal from direct state discounts under the 2007 Property Tax Credit Fund. It grew substantially after the Legislature added an income tax credit based on school district taxes in 2020 and on community college taxes this year. (Our figures assume these operations claimed those two credits — which hasn’t always been so statewide.)

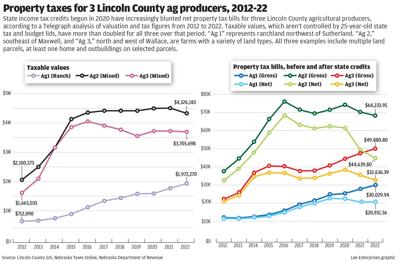

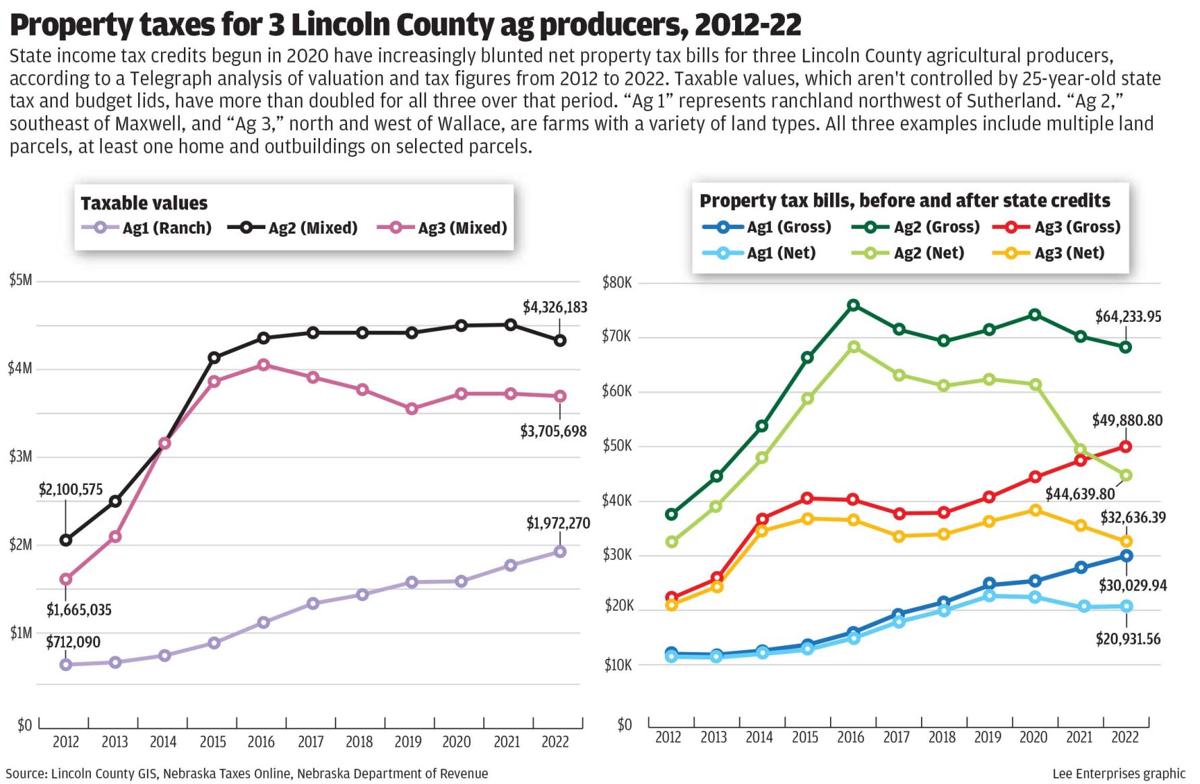

Total taxable values for all three operations have doubled or more since 2012. State lids control growth in tax rates and local budgets, but not taxable values.

However, only one of the three has seen an unbroken string of valuation increases. In fact, combined valuations for tax purposes have dropped recently for the other two.

The Telegraph chose its three sample operations by scouting out the county’s different regions on the Lincoln County GIS website (lincoln.gworks.com).

Our “Ag 1” operation consists of grassland in the cattle-growing Sandhills northwest of Sutherland. “Ag 2” includes a variety of soil types near the Platte River southeast of Maxwell, as does “Ag 3” north and west of Wallace.

Valuation information was available on Lincoln County GIS, while past tax information on the properties was gleaned from Nebraska Taxes Online (nto.us). Tax-credit information came from the Nebraska Department of Revenue (revenue.nebraska.gov).

We sought first to represent different areas of rural Lincoln County, as we did in choosing homes in different parts of North Platte four years ago to highlight in our regular local budget coverage.

County Assessor Julie Stenger answered some technical questions for us. But neither she nor her office had any input into which properties we chose, just as when we chose our three sample homes in 2018.

We aimed to choose one operation apiece within each of the county’s geographic predominant soil types —grassland, irrigated land and dryland — to reflect the different tax experiences of cattle ranchers and producers who primarily are farmers.

In practice, our “irrigated” and “dryland” choices include examples of all three major soil types. Ag 2 also has wasteland and accretion ground.

Each of these sample ag operations involve multiple parcels of real estate. Ag 1 has seven parcels, while Ag 2 and Ag 3 have eight parcels apiece.

Finally, all three have at least one residence and a varying number of outbuildings. Those are valued at 92% to 100% of actual value, like our three sample North Platte homes.

That’s one reason — beyond the obvious differences between farms and ranches — why ag producers’ tax experiences aren’t identical.

They may acquire additional parcels — as one did during the 2012-22 period — or sell others. Building new structures or demolishing others also could alter their total tax picture.

Their mix of soil types — and subtypes within the three major types — also matters. In a given year, the Assessor’s Office might raise taxable values for some while lowering others.

State law requires assessors or their staffs to physically inspect properties every six years. Stenger said her staff follows that rotation for ag operations’ homes or outbuildings, with the next round of inspections due in 2025.

For parcels with no buildings, aerial photos her office obtains every two years satisfy the legal physical inspection requirement, she said.

But ag properties’ taxable values remain driven by sales of similar types of land. Hot land markets drove ag valuations sharply higher last decade, as The Telegraph’s analysis shows.

Stenger said assessors must use a three-year average of similar land sales and set values between 69% and 75% of taxable value to satisfy state law.

The veteran assessor says she agonizes over the disconnection between what ag producers may be experiencing and state law’s reliance on land sales.

“Right now, when the economy is so poor and costs of food and fuel and fertilizer are so high, land sales are pretty stagnant right now,” Stenger said. “They’re stuck at that high valuation, which is unfortunate.”

But state law dictates everything her office does, she added. “Nebraska is a market-value state. There is no other option. That’s the law.”

The Nebraska Supreme Court, in a 1988 case involving North Platte’s mall (now District 177), struck down a 1984 law that allowed ag land to be valued for tax purposes based on its earning capacity. Some bordering states use a similar system.

Bills to restore the earning-capacity approach have failed, though Nebraska voters in 1990 allowed ag land to be valued differently than other land.

A 2019 attempt by state Sen. Steve Erdman of Bayard foundered, in part over differences over how to refine the earning-capacity formula from its 1984 version.

For Ag 1, the Sutherland-area grassland ag operation, both combined taxable valuations and gross property taxes have risen steadily over the 2012-22 period in the Telegraph’s analysis.

But even under the market-value system, combined taxable values for Ag 2 and Ag 3 — the Maxwell-area and Wallace-area operations — have slipped after steep inclines from 2012 to 2016.

Ag 3’s total valuation reached $4.06 million in the latter year but now stands at $3.7 million. Ag 2’s valuation reached $4.5 million in 2021 before falling to $4.33 million this year.

Those declines, however, haven’t entirely showed up in the two farm-based operations’ gross tax bills before state tax credits are accounted for.

Ag 2’s gross taxes, which were $33,977 in 2012, have twice topped $70,000 over the past decade. Its 2022 bill before credits is $64,234.

Ag 3’s gross tax bill dipped somewhat in 2017 and 2018 but had risen by this year to $49,881, more than twice its $22,397 total in 2012.

Only in the past two years, with the addition of the school and community college income tax credits alongside the older Property Tax Credit Fund, have The Telegraph’s three ag operations seen much tax relief from the state.

If its owners claim their income tax credits, grassland-based Ag 1’s net tax bill will be $20,932 this year. That’s 8.2% lower than in 2020 but nearly twice its 2012 level of $11,801 when just the older state discount existed.

Ag 2, the Maxwell-area operation, saw its 2012 net tax bill of $32,475 more than double to $67,980 by 2016. It’s now at $44,640 — 34.3% lower than six years ago — but was $62,006 in 2019 before the income tax credits started.

The Ag 3 operation near Wallace stands in the middle. Its net tax bill has grown from $21,206 a decade ago to $32,637 this year but was $38,334 in the school tax credit’s first year in 2020.

All Nebraska property owners can file for 2022 income tax credits equal to 30% of their K-12 school and community college tax bills for the same year. They’ll receive a refund check for those amounts even if they don’t owe income taxes for this year.