Successful investing requires more than just setting aside money every month. You also need a clear idea of your investment objectives and risk tolerance — and how those characteristics change over time. Investment decisions you make early in life won’t look like those you make as you close in on retirement.

As long as you have a grasp of these essential concepts, you can begin developing investment strategies by age that will help you reach your financial goals. Keep reading to learn about the 10 best places to invest your money now.

Why Invest?

It might be tempting to put all your money into savings accounts that are protected by the Federal Deposit Insurance Corporation, but that’s not a winning financial strategy over the long term. Investing in other assets like stocks, mutual funds and real estate helps you grow your money faster, save more for retirement, and achieve much higher returns than just parking your money in the bank.

The question then becomes which types of assets to invest in — and when. A good place to start is by understanding the various assets available for investment.

Types of Assets to Invest In

From a financial standpoint, assets are tools you can invest in as a way to build wealth. Different types of asset classes provide different returns and risks. The broadest categories of investment assets are growth and income. A growth asset, such as a stock, is designed to increase in value over time. An income asset typically generates a return by paying out income to investors, like with a bond or certificate of deposit.

Assets categorized by their risk characteristics are classified from conservative to moderate to aggressive. While conservative assets tend to offer the lowest potential return, they’re also the least likely to lose money. Aggressive assets such as growth stocks offer much higher potential returns but also carry much higher risk.

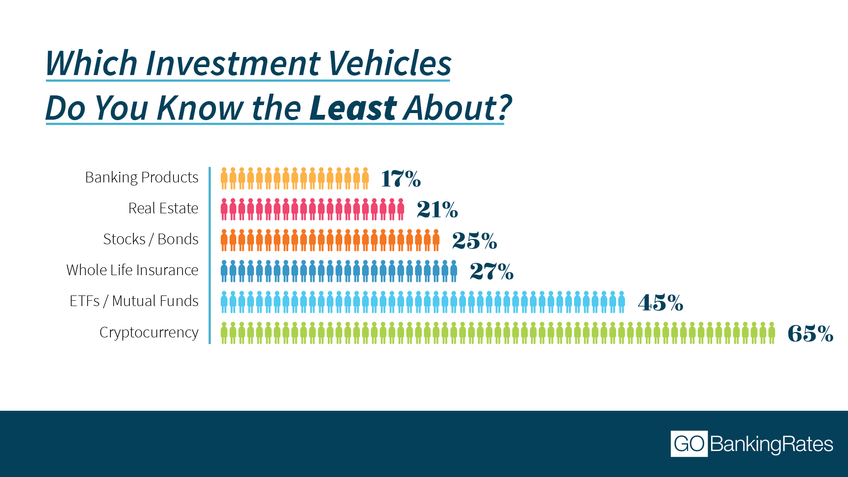

This survey done by GOBankingRates reveals some of the respondents’ feelings about the different types of investments.

Here is a look at the most popular investment options, followed by a rundown of how your portfolio and investment decisions will evolve as you get older.

1. Stocks

Stocks tend to be high on the risk/reward spectrum because you’re putting your money into a single company. But certain stocks carry more risk than others. For example, a biotech startup that only has one speculative product in development and no history of sales carries more risk than a so-called “blue chip” stock such as Coca-Cola, which has more than a century of history and consistent dividend payments. At the same time, riskier stocks also offer potentially greater returns.

2. Mutual Funds

Mutual funds are collective pools of money invested by professional fund managers on behalf of individual clients. Mutual funds cover essentially any asset class or risk profile you can imagine — from high-risk growth stocks to low-risk government bonds.

3. Index Funds

An index fund is a type of fund that tracks an underlying index, such as the S&P 500. The chief advantage of index funds is that they provide a low-cost way to diversify your portfolio while lessening the likelihood of losing some or all your money with individual stocks.

4. Exchange-Traded Funds

Exchange-traded funds trade on an exchange just like a stock. The difference is, ETFs hold multiple investments, just like other funds. Most ETFs are passively managed index funds, but not all are. Some are actively managed by professional fund managers. ETFs are typically low-cost investments that carry varying degrees of risk.

5. Bonds

A bond is an income investment. If you buy one at its face value, typically $1,000, you’ll receive that money back when the bond matures, which can be anywhere from a few months to a few decades. Along the way, you’ll receive regular interest payments, which are typically paid twice a year but might be more frequent. Bonds tend to be low-risk investments — especially U.S. Treasury securities, which are backed by the full faith and credit of the government.

6. 401(k) or 403(b) Plans

These are both employer-sponsored retirement plans that operate similar to mutual funds in that you can select your preferred asset allocations and risk levels. Contributions go in tax-free and assets grow tax-deferred until you withdraw your money in retirement. Along the way, your employer might match a portion of your contributions, which means you get free money. The key difference is that 401(k) plans are offered to employees of for-profit companies, whereas 403(b) plans are offered to employees of non-profit organizations and government bodies. [5] Keep in mind that you might face penalties if you withdraw funds before reaching age 59 1/2.

7. Roth IRAs

A Roth IRA is similar to other retirement accounts, except that instead of getting a tax deduction for your contributions, you can withdraw tax-free when you are retired. Roth IRAs are usually self-directed, meaning you open them up yourself with a broker rather than through an employer. With a Roth IRA, you can usually choose any type of investment you’d like, from stocks and bonds to index funds and mutual funds.

8. Real Estate

Real estate can be a very active investment — especially if you buy the property yourself to earn rental income or to flip for a profit. A more passive option is to invest in a real estate investment trust, or REIT, which packages various types of real estate portfolios and trades on the stock exchange. Real estate of any type can be a useful diversification tool, as real estate prices don’t move in lockstep with stocks or bonds.

9. High-Yield Savings Accounts

A high-yield savings account is an FDIC-insured investment that is very safe but offers a high annual percentage yield compared to traditional savings accounts. For example, as of May 2021, the national average APY on savings accounts was only 0.07%, according to FDIC data. In contrast, the highest-yield savings accounts offer APYs of 0.70% and higher.

10. Money Market Accounts

A money market account is another form of cash alternative that can be a safe place to earn a modest return on your investments. True money market accounts also carry FDIC insurance and can pay yields comparable to some high-yield savings accounts. These are conservative investments that keep your money safe while earning you a small amount of interest.

Investment Strategies By Age

Once you are familiar with the types of accounts and assets you can invest in, the next step is to figure out which of these assets make the most sense as you get older. Here’s a quick primer on the best investment strategies by age group:

Investment Strategies by Age Group

- 20s: When you’re just starting as an investor, you can afford to take more risks because you have plenty of time to recover from any big losses. This is the period to allocate a larger percentage of your portfolio in high-growth stocks that carry more risk but have a bigger potential upside.

- 30s: In your 30s you start to earn more money while also being decades away from your retirement date. At this stage, you can still be aggressive with your investments. You also stand to earn strong returns because you should have more money available to invest than when you were in your 20s.

- 40s: This is the stage of life when you’re nearing your peak earning years, so it’s a good time to max out your 401(k) or 403(b) plans. Although you are still a decade or more away from retirement, you want to lower the risk in your portfolio by allocating more money toward bonds and savings accounts.

- 50s and beyond: If you’ve invested successfully before you reach your 50s, retirement should be in plain view. In this case, it makes sense to dramatically downshift the risk in your portfolio so that you don’t lose your nest egg right before you need it. Move more money toward safe investments like bonds, money market accounts, low-risk funds and blue-chip stocks, and away from high-risk growth stocks.

Vance Cariaga contributed to the reporting for this article.